All Categories

Featured

Table of Contents

Note, nevertheless, that this doesn't claim anything about changing for inflation. On the bonus side, also if you think your choice would be to invest in the securities market for those seven years, and that you 'd obtain a 10 percent annual return (which is far from certain, particularly in the coming decade), this $8208 a year would be greater than 4 percent of the resulting small stock value.

Example of a single-premium deferred annuity (with a 25-year deferral), with four settlement alternatives. Politeness Charles Schwab. The regular monthly payment here is greatest for the "joint-life-only" alternative, at $1258 (164 percent more than with the prompt annuity). The "joint-life-with-cash-refund" choice pays out only $7/month much less, and guarantees at the very least $100,000 will be paid out.

The way you acquire the annuity will certainly identify the response to that concern. If you acquire an annuity with pre-tax dollars, your premium decreases your taxable revenue for that year. According to , acquiring an annuity inside a Roth plan results in tax-free repayments.

How do I receive payments from an Annuity Income?

The expert's first step was to create an extensive monetary strategy for you, and after that clarify (a) just how the suggested annuity matches your general strategy, (b) what choices s/he thought about, and (c) just how such alternatives would or would not have resulted in lower or higher compensation for the expert, and (d) why the annuity is the premium choice for you. - Flexible premium annuities

Naturally, a consultant may try pressing annuities even if they're not the most effective suitable for your situation and objectives. The factor could be as benign as it is the only item they market, so they drop target to the proverbial, "If all you have in your tool kit is a hammer, quite soon everything begins resembling a nail." While the advisor in this circumstance may not be unethical, it increases the danger that an annuity is an inadequate option for you.

Annuity Riders

Because annuities frequently pay the agent selling them much greater commissions than what s/he would certainly get for investing your money in mutual funds - Annuity income, not to mention the absolutely no compensations s/he 'd get if you purchase no-load mutual funds, there is a large motivation for agents to press annuities, and the more challenging the better ()

An unscrupulous expert recommends rolling that amount right into new "better" funds that simply take place to carry a 4 percent sales load. Agree to this, and the advisor pockets $20,000 of your $500,000, and the funds aren't likely to perform far better (unless you selected much more improperly to start with). In the exact same example, the expert could guide you to buy a challenging annuity keeping that $500,000, one that pays him or her an 8 percent compensation.

The advisor attempts to rush your decision, declaring the deal will certainly soon go away. It might indeed, yet there will likely be equivalent deals later. The expert hasn't identified just how annuity payments will be tired. The expert hasn't revealed his/her compensation and/or the charges you'll be charged and/or hasn't shown you the impact of those on your eventual payments, and/or the settlement and/or costs are unacceptably high.

Current rate of interest prices, and thus predicted settlements, are traditionally low. Also if an annuity is appropriate for you, do your due diligence in contrasting annuities marketed by brokers vs. no-load ones sold by the issuing company.

Can I get an Fixed Vs Variable Annuities online?

The stream of monthly settlements from Social Protection is comparable to those of a postponed annuity. Because annuities are voluntary, the individuals acquiring them typically self-select as having a longer-than-average life expectations.

Social Security advantages are totally indexed to the CPI, while annuities either have no rising cost of living security or at a lot of provide an established percent yearly boost that might or might not make up for inflation in complete. This type of cyclist, as with anything else that boosts the insurance firm's risk, requires you to pay more for the annuity, or accept reduced settlements.

What are the benefits of having an Lifetime Payout Annuities?

Please note: This article is meant for educational purposes only, and ought to not be considered economic guidance. You need to get in touch with a monetary specialist prior to making any significant financial choices.

Given that annuities are intended for retirement, taxes and fines might apply. Principal Security of Fixed Annuities.

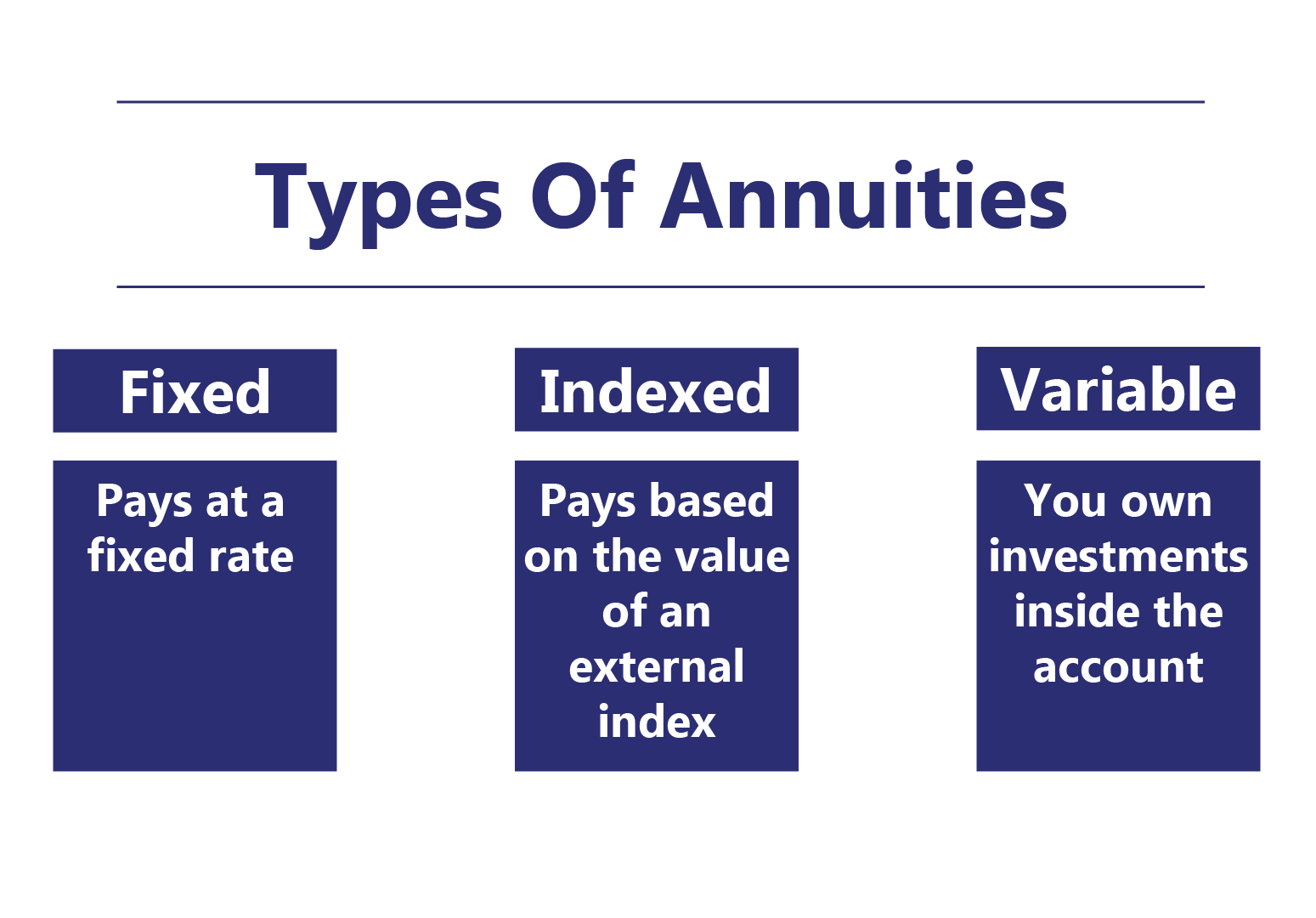

Immediate annuities. Made use of by those that want trustworthy revenue quickly (or within one year of purchase). With it, you can tailor revenue to fit your needs and produce revenue that lasts for life. Deferred annuities: For those that intend to expand their money in time, however want to delay access to the cash till retired life years.

How do Retirement Annuities provide guaranteed income?

Variable annuities: Provides higher possibility for growth by spending your money in financial investment choices you choose and the ability to rebalance your profile based on your choices and in a way that straightens with changing monetary objectives. With repaired annuities, the firm spends the funds and offers a rates of interest to the customer.

When a death claim accompanies an annuity, it is necessary to have a named recipient in the agreement. Different alternatives exist for annuity fatality benefits, depending on the contract and insurance company. Picking a refund or "duration specific" option in your annuity gives a survivor benefit if you pass away early.

What is included in an Annuity Withdrawal Options contract?

Naming a recipient other than the estate can help this procedure go much more smoothly, and can help make sure that the proceeds go to whoever the private desired the money to go to rather than going through probate. When present, a death benefit is immediately included with your contract.

{kind=link}

Table of Contents

Latest Posts

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Investment Choices Breaking Down the Basics of Deferred Annuity Vs Variable Annuity Features of Smart Investment Choices

Breaking Down Your Investment Choices Key Insights on Fixed Income Annuity Vs Variable Annuity Defining Annuities Fixed Vs Variable Features of What Is A Variable Annuity Vs A Fixed Annuity Why Fixed

Analyzing Fixed Annuity Or Variable Annuity A Comprehensive Guide to Pros And Cons Of Fixed Annuity And Variable Annuity What Is What Is A Variable Annuity Vs A Fixed Annuity? Features of Fixed Income

More

Latest Posts